(Community Matters) Everyone always asks, what are you going to do in Marfa for three weeks –

. . . . about mine & Steven’s relationship, our work in the world, two or three distinct, 3 – 5 year scenarios of our operating environment, the Entrepreneurs Foundation, our CSR conference in February, St. James Episcopal Church and our missions, Fuse Box Festival & how I can help, PeopleFund & PeopleTrust, what I should be doing for the Obama administration, RISE, the Acton session I’ve agreed to lead in February, the two plays I’ve been thinking of producing next year, investments & forecasts, my role as a board member for the KDK-Harman Foundation, my role as a (now) former governor for the Austin Community Foundation, affordable housing for Austinites, city council elections, the governor’s race, the US Senate race, our families (parents, siblings, nieces/nephews, god children, closest friends) so much to think about in so little time. Most of this gets touched by reading and discussing economics, politics and history. And, I’ll leave Marfa with at least a few written notes for each – lots for some.

We’ll decompress . . .

Part of the magic of Marfa is the 6 to 7 hour drive from Austin. It’s not like driving north, east or south. There’s hardly any traffic driving west. Most of the time the road is empty, straight and long. Neither of us napped, nor hardly read. We talked. It’s the equivalent of spending 2 or 3 days together. We hit on all sort of issues – agreed, argued, acted lovey dovey and fought. Then you turn off I-10 onto 67 through Alpine, into Marfa.

We’ve only been here 34 hours and already we’ve cooked twice, taken walks, taken naps, unpacked two large boxes of books, weeks of not-fully-read Economists, stacks of articles passed on from others, a five inch thick binder on corporate social responsibility and are sharing the best of what we read with each other. I won’t dive into work for a week, though both consciously and unconsciously I’m further creating the frames for next year through which I’ll interpret the extraordinary amount of information the staff has organized.

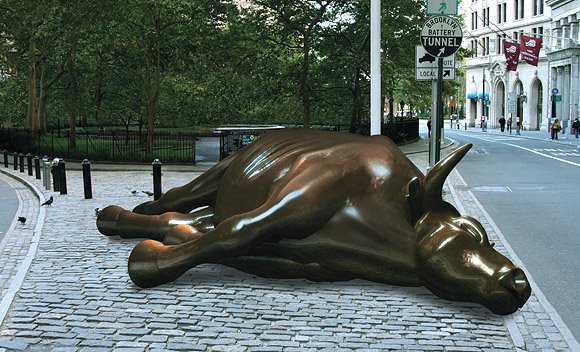

One of the pieces I read yesterday: Michael Lewis wrote, Liar’s Poker, and has now written The End. which is about what went wrong on Wall Street. I recommend this article to you. It’ll inform my financial scenarios. Excerpts:

I’d never taken an accounting course, never run a business, never even had savings of my own to manage. I stumbled into a job at Salomon Brothers in 1985 and stumbled out much richer three years later.

Then came Meredith Whitney with news . . . . a woman whom basically no one had ever heard of had shaved $369 billion off the value of financial firms in the market. For better than a year now, Whitney has responded to the claims by bankers and brokers that they had put their problems behind them with this write-down or that capital raise with a claim of her own: You’re wrong. You’re still not facing up to how badly you have mismanaged your business. This woman wasn’t saying Wall Street was corrupt. She was saying they were stupid.

(while interviewing one of the, now, celebrated short sellers of Wall Street) ‘What I learned from that experience was that Wall Street didn’t give a shit what it sold.’ Thought Alan Greenspan’s decision after the internet bust to lower interest rates to 1 percent was a travesty that would lead to some terrible day of reckoning.

The juiciest shorts – the bonds ultimately backed by the mortgages most likely to default-had several characteristics. They’d be in what Wall Street people were now calling the sand states: Arizona, California, Florida, Nevada.

How much did home prices need to fall for these loans to blow up? (it turned out they didn’t have to fall; they merely needed to stay flat).

Eisman knew subprime lenders could be scumbags. What he underestimated was the total unabashed complicity of the upper class of American capitalism. For instance, he knew that the big Wall Street investment banks took huge piles of loans that in and of themselves might be rated BBB, threw them into a trust, carved the trust into traunches, and wound up with 60% of the new total being rated AAA.

By selling shorts in the bonds, the investment houses created identical income streams without the actual assets, ‘they were creating them out of whole cloth. One hundred times over! That’s why the losses are so much greater than the loans. But that’s when I realized they needed us to keep the machine running.’

‘He explained that the rating agencies were morally bankrupt and living in fear of becoming actually bankrupt.’ Their financial models didn’t even allow for any decrease in housing prices.

By going public the investment banks ‘transferred the ulimate financial risk from themselves to their shareholders.’ ‘No investment bank owned by its employees would have levered itself 35 to 1 or bought and held $50 billion in mezzanine C.D.O.’s I doubt any partnership would have sought to game the rating agencies or leap into bed with loan sharks or even allow mezzanine C.D.O.’s to be sold to its customers. The hoped-for short-term gain would not have justified the long-term hit.

As a board member of several organizations, the CEO of another and for our own plans, I’ve been wrestling with firming up financial scenarios.

A year ago, I asked the staff of one organization on whose board I sit to prepare contingency plans for an unprecendented financial downturn and the resulting increases in loan losses. This solicited more than a few rolled eyes from staff and fellow board members so I didn’t pursue the request as much as I would have liked, though we did some planning & preparation which has served us well.

Last month, I asked the staff to imagine our clients’ revenues decreased by 25% and 50% and stayed at these levels for the next 25 years. Of course, I don’t anticipate 25 years but I was trying to make a point that business operating plans shouldn’t assume our economic downturn will be short lived. It’s my belief that those organizations which most conservatively manage risk will prepare for and be able to withstand a prolonged recession – especially a double dip recession since hyper-inflation and the resulting economic policy to deal with it (let’s not forget Volcker has our new president’s ear) are favored given the new money supply. And, there are certain undercapitalized businesses which should be liquidated or mothballed. One of my memories as a banker in the 80’s is that I didn’t do certain customers any good by lending them more money to hold on, which wasn’t successful and which simply dug a deeper hole.

Entering this reflective time, my best case scenario is the downturn becoming worse post-inauguration, only leveling off after 24 months, either flat or in slow recovery year 3.

I’ve listened to optimistic scenarios which assume that as a result of the extraordinary supply of idle money, recovery will be much quicker. I’d rather jump in late than sit on my board for months or years in shark infested waters waiting on that wave.

Nevertheless, identifying opportunities during the downturn is critical, especially as relates to PeopleTrust (our land trust to promote affordable housing) and Steven and my investment plans.